Sarah Pulkowski

President, Towson University Investment Group

Jacob Piazza

Portfolio Manager, Towson University Investment Group

Keyur Patel

Vice-President, Towson University Investment Group

Aleksandr Olshanskiy

Compliance Officer, Towson University Investment Group

Introduction

The Towson University Investment Group (TUIG) conducted

a survey concerning the extent to which Towson

University students have knowledge of retirement and

financial planning concepts. Basic demographic and education-

related information was first queried, followed

by retirement planning and respondents’ knowledge

of available financial instruments. In total, we had

26 respondents. With the existing macroeconomic

backdrop as it currently stands – divergence between

the S&P 500 and SMID cap equities, and treasuries

at an all-time low after accommodative actions by the

Fed – retirement planning, we surmised, is especially

important for new college graduates. Key questions

in the survey included: When do you want to retire?

How much do you need to retire? What percent of

your income do you save for retirement each year?

How much money do you expect to live on each year

while in retirement?

Towson University is composed of the following colleges:

College of Business & Economics (CBE), College

of Health Professions (CHP), Jess & Mildred Fisher

College of Science & Mathematics (FCSM), College

of Liberal Arts (CLA), College of Fine Arts & Communication

(COFAC), and College of Education (CE).

The students questioned were segmented by college.

Allowing for inter-college and intra-college comparisons.

In addition to segmenting students by college,

we also segmented students by major. We conducted

the survey in October 2020. With the results of the

survey, we were able to show how Towson University

students are preparing for retirement, and their overall

knowledge of retirement.

Participant Background

The demographics data from our respondents indicates

no particular skew to any given population; 53.6% of

our participants are between 20-21, while 53.6% are

male. In terms of ethnic distribution, respondents were

28.6% Black/African American and 32.1% Caucasian,

with the remainder being distributed between Hispanic,

Asian, and Native American ethnic groups. We saw a

moderate skew towards older students, with more than

80% of respondents having more than 60 credits (Junior

and Seniors), which we believe is more applicable to our

initial goal of evaluating college graduates’ knowledge

of retirement planning concepts.

In seeking to evaluate the sources of retirement planning

knowledge, and the potential impact of education

by parents, we asked respondents the extent of their

parents/ education. More than 80% of respondents’

parents have earned undergraduate degrees or gone on

to complete post-graduate education, while only 15%

of respondents’ parents had high school diplomas. As

graduates of higher education make, on average, more

income than those having only graduated high school,

we concluded that respondents had a clear skew towards

belonging to middle to higher income households. As

for respondents’ employment, more than 70% were

employed or interning in some capacity. Of the 70%

employed, the majority were employed for wages, either

salaried or paid by the hour.

While students from every college were among the

respondents (save Education), there was a preponderance

of students from the College of Business &

Economics (CBE). Over 15 students from CBE answered

our survey, the majority of which are majoring in

Finance or Financial Planning. The average GPA for

respondents was 3.25, with a range between 2.1 and 4.0.

Retirement Planning

Of our samples, 21.4% of respondents stated they

plan to retire at the age of 65. The average and median

planned retirement age, 55 and 60 years old, respectively,

indicated that, on average, students planned to

retire five years or more before the full retirement age.

Despite the full retirement age for individuals born

after 1960 increasing to 67, TU students plan to retire,

on average, at 55 years of age. TU students’ average

planned retirement age is also 7 years before they are

entitled to begin receiving social security payouts. At

age 62, the earliest that an individual can receive social

security benefits, only 70% of the social security benefits

are received. By retiring early, the accumulation period

is reduced while the distribution period is increased,

creating the real risk that a retiree will outlive their

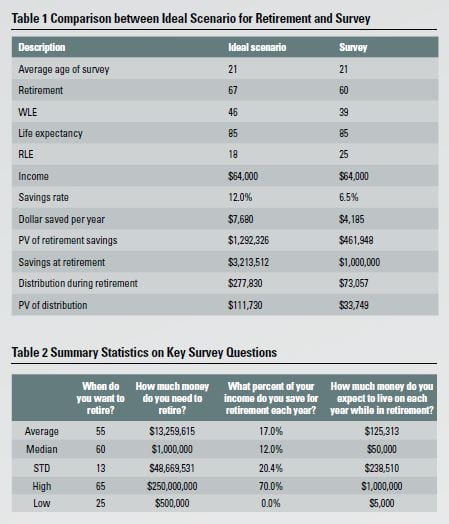

retirement savings. Table 1 presents a comparison

between the ideal scenario for retirement planning and

the situation based on our survey.

We report the summary statistics of key survey questions

in Table 2. The median and average savings respondents

indicated as being sufficient for retirement were

$1,000,000 and $13,300,000, respectively. As far as

yearly cash flow needed in retirement, on average

respondents stated that they would need $125,000 in

retirement. These numbers conclude that students need

to make sure they create or have a long-term retirement

plan created that is updated and monitored for them

to achieve retirement success.

Towson University’s Financial Planning coursework

teaches basic calculations required for retirement planning.

If a person states to save early in life for retirement,

with an appropriate savings rate, they can accumulate

enough savings for a comfortable retirement. The ideal

scenario’s saving rate for a person in their early twenties

is 11%-13%.

With answers varying from $500,000 to $20,000,000,

students have a wide range of expectations for savings

required to retire. The majority of the respondents said

they will save $1,000,000 in preparation for retirement.

With the assumption of 2% inflation and 8% annual

return on the investment, this gives inflation adjusted

return of 5.88% during their retirement. Based on

the previous assumptions, if they save $1,000,000

by the time they retire, individuals will have $73,057

of annual distributions from their portfolio during

retirement. The present value of the expected annual

spending is $33,749. This return is based on aggressive

investing even during retirement. These calculations

should be reviewed with consideration that a modest

change in inflation, retirement life or return on the

portfolio will have dramatic effect on the disposable

income of a retiree.

Additionally, 10.7% of students have not saved anything

for retirement. Since reviewing the survey results and

expectations of retirement income, we see that most

students are not seriously preparing for retirement.

Standard guidelines of financial planning state that,

in order to retire, one must save at least 10% of their

annual income.

In addition to consistently saving income, retirement

account strategies should be considered while planning

for retirement. We surveyed students on their expectations

regarding tax rates and their knowledge on the

relation between tax and social security. Overall, students

predict an increase in taxes due to inflation and

the overall long-term impacts of Covid-19. Students

at Towson University have a broad understanding

of how this government funded retirement program

works, perceiving it to be the following1: “Social Security

is government provided disability and retirement

income. For most citizens, after the age of 75, one can

receive social security. Before then, social security taxes

6.2% are taken out of each paycheck for employed

individuals. It is a form of compensation for older

citizens, citizens with disabilities, and citizens that

are widow(er)s.” Social security benefits, in actuality,

can be received as early as 62 (with penalties), and by

67 without penalties. Each individual’s social security

benefits vary depending on how much they earned and

how long they contributed to social security. 14 out of

26 respondents (53.9%) were able to correctly answer

basic questions regarding Social Security, while the

remaining had no knowledge or with misconception.

Though many students do not have a complete knowledge

of retirement, nor have they adequately planned

for retirement, 76% of students indicated that they will

seek financial planning advice in the future. Seeking the

advice of a Financial Professional will help to ensure that

one will be able to enjoy their golden years and possibly

extend the number of golden years an individual may

enjoy. The answers provided by students demonstrate

that those who are studying finance related subjects

have an excellent understanding of Social Security,

Retirement Planning, and Alternative Investments. The

survey conducted by the Towson University Investment

Group finds that Towson University is producing individuals

who are capable, well educated, and aware of

the current economic and financial market conditions.

Towson University is producing individuals who can

network and rely on each other to meet the demands

of knowledge that all aspects of life require, including

financial planning and retiring.

1Definition was created by compiling the correct or partially correct

answers from respondents.