Babu G. Baradwaj

Professor, Department of Finance, Towson University

Michaël Dewally

Associate Professor, Department of Finance, Towson University

Susan M.V. Flaherty

Professor, Department of Finance, Towson University

Yingying Shao

Associate Professor, Department of Finance, Towson University

Banks, as financial intermediaries, transform risk. They take riskless deposits to finance risky loans. The resulting mismatch between the maturity of deposits and loans exposes banks to interest rate risk: unexpected changes in interest rates impact banks’ performance. When interest rates are volatile and hard to predict, banks must manage interest rate risk effectively to protect capital and prevent insolvency.

While it is crucial for banks to carefully assess and manage their exposure to interest rate risk, there is no theoretically optimal solution for banks to determine the desired level of their risk exposure. Banks, in general, are willing to assume interest rate risk to a certain extent to increase their profitability, especially when the yield curve shifts.

Traditionally, banks rely on active management of the maturity gap to control interest rate risk. With the development of financial innovations, more and more banks have adopted off-balance-sheet activities such as using interest rate derivatives to manage their interest rate risk. In light of these considerations, it is important to know to what extent banks rely on interest rate derivatives and thus evaluate their ability to adjust their interest rate risk exposure.

How do Maryland Banks

Manage their Interest Rate Risk?

We aim to: (1) quantify interest rate risk and examine how it changed over time and (2) assess how banks manage their interest rate risk exposure. Banks control their exposure by either modifying the maturity mismatch between on-balance-sheet assets and liabilities (on-balance-sheet restructuring) or relying on interest rate derivatives (off-balance-sheet adjustment). Most of Maryland banks are relatively small in asset size and follow a traditional business model. Their exposure to interest rate risk impacts their performance including both profitability and solvency. We also investigate if Maryland banks behave differently than other banks in the nation.

Using data from banks’ quarterly Call reports between 2000 and 2016, we measure interest rate risk exposure in two ways. This first measure is “maturity GAP”, computed as the difference in 12-month maturity between the banks’ assets and liabilities divided by total assets (Sierra and Yeager, 2004). The difference or GAP between interest rate sensitive assets and liabilities can be multiplied by a forecasted change in interest rates to approximate the change in net interest income. Banks take deposits and issue loans in various terms and rate structures, e.g., fixed-rate vs. floating-rate instruments, whose impact on the economic value of banks is different. When the interest rate increases, a bank that finances fixed-rate, long-term loans with short-term deposits will suffer a decline in profits because the interest income from loans remains fixed yet the cost of funds increases. Using this approach, a bank with a positive on-balance-sheet maturity gap is viewed as an asset-sensitive bank and those with a negative maturity gap as liability-sensitive, and a lower maturity mismatch corresponds to higher risk management activities. It should be noted that banks will position their balance sheets based on their forecast of interest rates. Positive gap (asset sensitive) balance sheets may increase net interest income during a rising interest rate environment while negative gap (liability sensitive) balance sheets may increase net interest income during a falling interest rate environment.

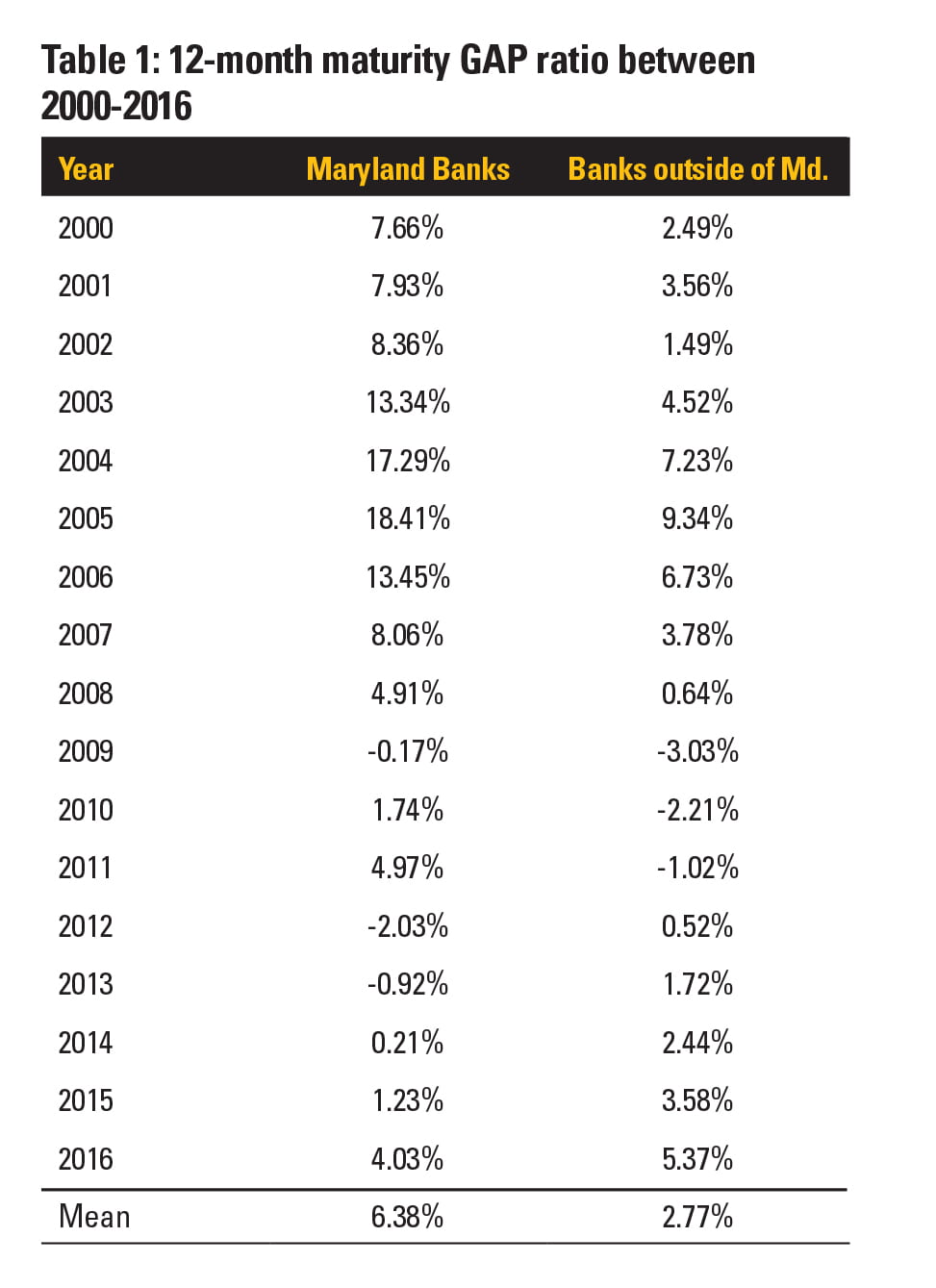

Table 1 provides summary statistics of the 12-month maturity GAP as a measurement of interest rate risk management for commercial banks from 2000–2016. Overall, banks in Maryland show a significantly higher level of GAP ratio compared to the average of other banks in the nation, indicating a lower level of management of interest rate risk. However, this situation has changed greatly after the 2007-2009 crisis as Maryland banks show a great drop in the GAP ratio, leading to a lower level ratio than banks in other states. The 2000-2006 average difference of outside- to inside-Maryland GAP ratio of 7.30% dropped to -0.17% for the 2010-2016 period. Maryland banks are now more insulated from interest rate risk.

The second measure is based on banks’ position in “derivatives used for hedging purposes” (Purnanandam, 2007). For each bank, we take the notional amount of derivatives reported under the non-trading purposes and scale it by the total assets of the bank at the end of each quarter.

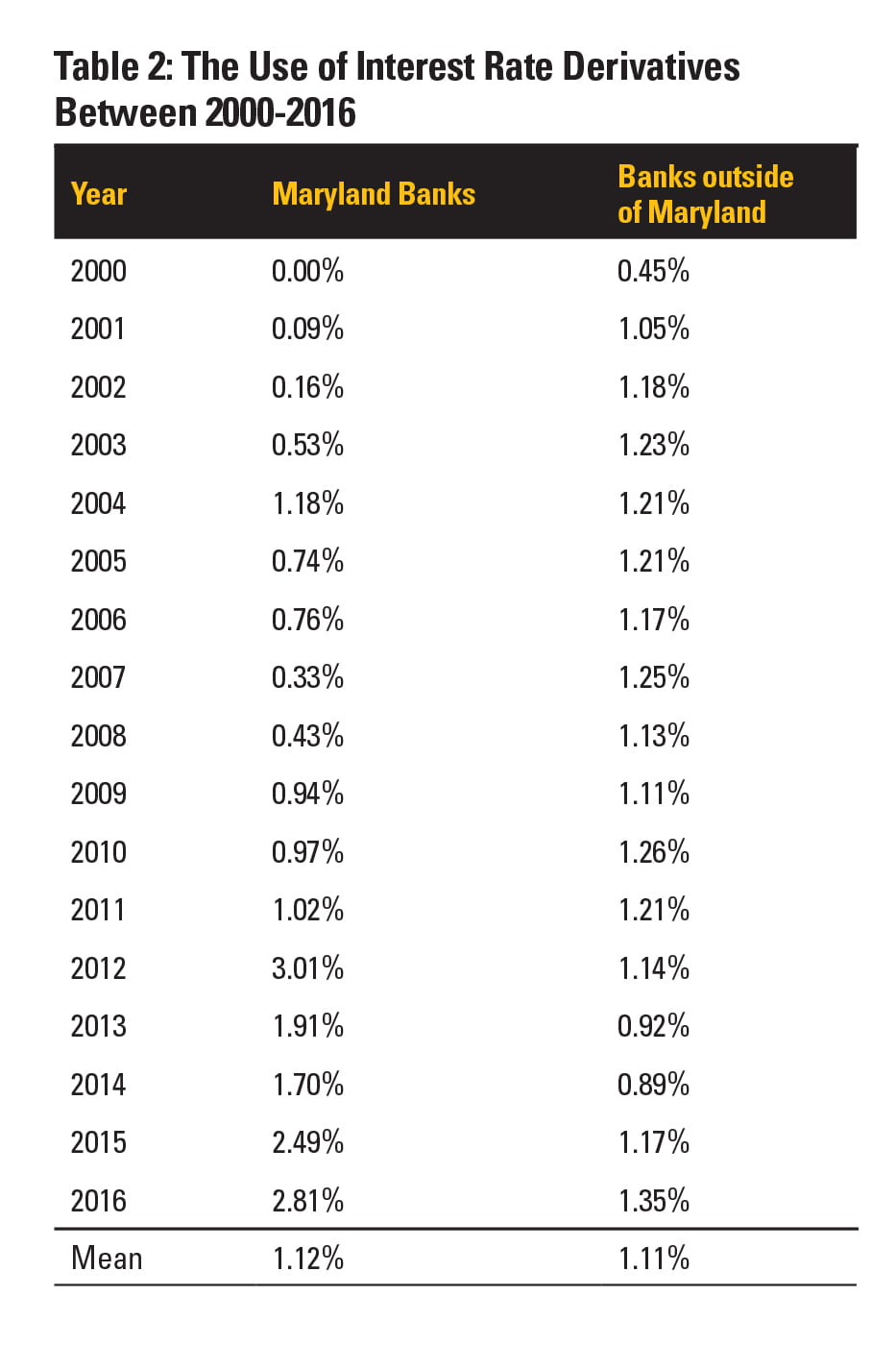

Table 2 provides summary statistics of the interest rate derivatives used for interest rate risk management purposes by commercial banks from 2000–2016. It is clear from this table that Maryland banks have become more active in managing interest rate risk since the financial crisis. The average hedging ratio of Maryland banks in the years since 2009 has significantly outpaced the hedging ratio of banks in other states. Maryland banks’ average hedging ratio for 2010-2016 is 1.99% compared to an average of 1.13% for banks outside of Maryland. This finding is consistent with that of Table 1 whereby Maryland banks are currently actively controlling for interest rate risk.

Business Model

Are the differences noted above related to banks’ financial conditions and business models?

Table 3 reports statistics to help us compare the performance of Maryland banks to that of other banks in the nation. While Maryland banks are in general smaller than banks in other states, they show a higher level of loan ratio, lower level of demand deposits, and a similar level of capital reserve. In addition, Maryland banks seem to underperform other banks in terms of ROE, nonperforming loans, and liquidity conditions. This is consistent with the findings in the literature that banks with higher probability of financial distress manage their interest rate risk more aggressively, both by means of on-balance sheet and off-balance sheet instruments (Purnanandam, 2007).

In practice, banks manage interest rate risk primarily via their on-balance-sheet maturity structure and then decide whether to rely on interest rate derivatives as alternative tools. We conduct a test to examine to what extent banks’ use of interest rate derivatives is determined by banks’ on-balance-sheet maturity gap as the following:

Derivatives=α+β1 GAP+β2 Size+β3 Equity+β4 TLoan+β5 ROE+β6 NPL+β7 Liquidity+β8 FundRate+T+S+ε,

where Size is the logarithm of total assets, NPL is the ratio of loans over 90 days late plus loans not accruing to total loans, and Liquidity is defined as (Cash + Fed Funds Sold + Securities) divided by total assets. Fund Rate is the federal funds rate and measures the changes in interest rate over time.

We are particularly interested in the sign of coefficient β1. A negative (positive) value suggests that banks have used interest rate derivatives to substitute (complement) the on-balance-sheet exposure to interest rate risk.

The results in Table 4 show that Maryland banks use interest rate derivatives as a complement to traditional maturity gap matching in managing interest rate risk. On the contrary, banks outside of Maryland, in general, substitute one strategy for the other.

In addition, we run subsample tests using the time windows before 2007 and after 2010 respectively to see whether banks change interest rate risk management strategies significantly after the 2007-2009 financial crisis. The following table reports the value of regression coefficients only.

Table 5 shows that while Maryland banks have been consistently using interest rate derivatives as complementary to the traditional maturity matching approach in managing interest rate risk, other banks in the nation, in general, have been operating differently. Before the crisis, non-Maryland banks used off-balance-sheet interest rate derivatives as a substitute to on-balance-sheet interest rate risk management and only have switched the role of interest rate derivatives after the crisis.

While our findings document a response to the crisis, further study is required to determine how bank behavior is changing due to this protracted period of low long-term interest rates. Banks exhibit better performance when long-term rates are higher than shorter rates. Currently, long-term rates are negligibly higher than short-term rates. As banks adapt to a continual low rate environment, banks may take on more risk to generate yield which may increase derivative usage. This would further exacerbate the difference in derivative use between Maryland banks and those outside of Maryland.

References

Purnanandam, A., 2007. Interest rate derivatives at commercial banks: an empirical investigation. J. Monet. Econ. 54 (6), 1769–1808.

Sierra, G.E., Yeager, T.J., 2004. What does the federal reserve’s economic value model tell us about interest rate risk at U.S. community banks. Fed. Res. Bank St. Louis Rev. 86 (6), 45–60.